Business, Strategy, and Integration: Tamy Tanzilli's Contribution to CCIFB-SP

With almost 30 years of experience in international legal advisory, the SME Director of CCIFB-SP and Founding Partner of GTLawyers, Tamy Tanzilli, highlights how the Chamber is reinventing itself to better support small and medium French companies in Brazil — through qualified networking, structured governance, and strategic communication.

As the Director, she emphasizes key priorities: increasing benefits, strengthening value delivery for members, and fostering connections that truly generate business opportunities.

Check out the full article on the CCIFB website: https://abrir.link/CUkmM

THE TAXATION OF PROFITS AND DIVIDENDS DISTRIBUTED TO RESIDENT INDIVIDUALS WILL FOLLOW THE FOLLOWING RULES:

Taxation exclusively within the scope of the Minimum IRPF (Individual Income Tax) - focusing on high incomes:

Imposition of a Withholding Income Tax (IRFonte) at a rate of 10% on monthly distributions exceeding R$ 50 thousand ;

Requirement for an adjustment to the Annual Adjustment Declaration, considering:

- The sum of annual income exceeding R$ 600 thousand or R$ 1.2 million ;

- The minimum IRPF in the Annual Adjustment must exclude capital gains, accumulated income, and donations/inheritances ;

- The minimum IRPF will vary from 1% to 10%, depending on the income bracket ;

- The following can be deducted from the minimum IRPF: the IRPF due in the Annual Adjustment Declaration, the IRFonte withheld during the period (on income subject to minimum IRPF), and the definitive IRPF (also on amounts taxable by the minimum IRPF).

For dividends: Integration with the effective corporate income tax burden (IRPJ/CSLL), with the application of reducers if the minimum IRPF rate combined with IRPJ/CSLL exceeds 34%, 40%, or 45%, depending on the company type.

THE TAXATION OF PROFITS AND DIVIDENDS DISTRIBUTED TO NON-RESIDENTS WILL FOLLOW THESE RULES:

Taxation by IRFonte at 10 % at the moment of payment, credit, remittance, delivery, or employment.

Integration with the company's effective IRPJ/CSLL burden: Should the sum of the company's effective IRPJ/CSLL rates plus the IRFonte exceed the sum of the nominal IRPJ/CSLL rates (34 %, 40 %, or 45 %), a credit right will be granted within 360 days from the end of each fiscal year.

The credit must be equivalent to the difference between the effective IRPJ/CSLL rate, plus the 10 % IRFonte, and the nominal IRPJ/CSLL rate (34 %, 40 %, or 45 %, depending on the company's activity).

POINTS OF ATTENTION

- Taxation of results accrued until December 31, 2025: Maintenance of the current exemption, provided that their distribution was approved until December 31, 2025, and payment occurs under the terms originally stipulated in the approval act.

- Regulation of the credit right for non-resident investors.

- Capital increase with profits and dividends and maintenance of taxation.

- Impacts related to operating profit (SUDAM/SUDENE), Lei do Bem (Goodwill Law), PAT, incentivized depreciation, goodwill amortization, tax losses, interest on equity, and others. goodwill, prejuízos fiscais, juros sobre capital próprio e outros.

- Amendments to Bill 1.087 will be subject to a new bill, offering opportunities for adjustments and improvements to the tax regime established for dividends.

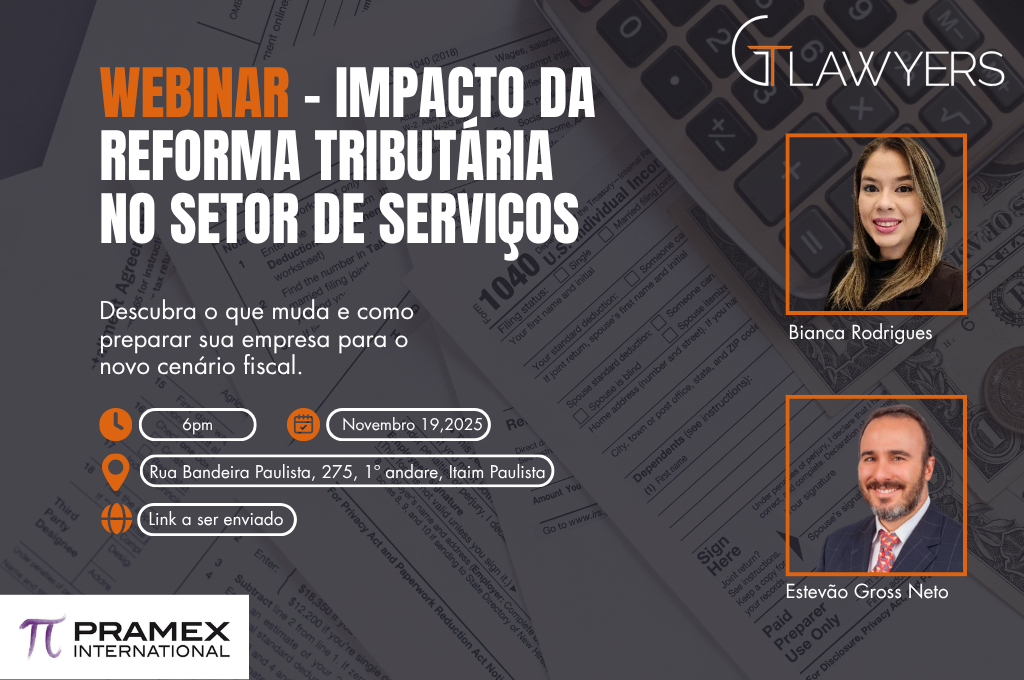

The Tax Reform is bringing profound changes with the implementation of CBS and IBS. Is your company prepared?

Join us in this webinar with our associate Estevão Gross and Bianca Rodrigues from Pramex International to understand:

✔️ The main changes brought by CBS and IBS.

✔️ How these changes impact the services sector.

✔️ Strategies for adaptation and tax planning.

🗓 When? November 19, 2025, at 6:00 PM

📍 Hybrid format: In-person (GTLawyers) and online

Sign up for free at the link: https://forms.office.com/Pages/ResponsePage.aspx?id=P4y0RUBc8UKE1BPJQMeTQMdGbSvlNA5AjWoGZX5ZMP1UQzNMOTNUMFNFTzBOM1VSWExGMUI0TVIzRi4u

A part of our French team, Cécile Verdeaux and Jeanne Puech, participated in the second day of the Journées Franco-Brésiliennes, held today, November 11th, at the USP Law School!

It was a day full of learning and knowledge exchange, featuring lectures and discussions on continental law, legal education in France, and the rich history of the Association Henri Capitant in Brazil.

Proud to be part of this journey of knowledge!

Last Monday, October 30, we had the privilege of attending the remarkable Gala Dinner and 2025 Personality Award of CCIFB-SP. This event celebrated 200 years of diplomatic relations between France and Brazil, as well as the 125th anniversary of the France-Brazil Chamber of Commerce - CCIFB.

Being present at such an evening reinforces our commitment to serving as a bridge between the legal and business worlds of two countries that share a strong and historical economic partnership. With over 1,300 French companies operating in Brazil, generating hundreds of thousands of jobs, the potential of this synergy continues to inspire!

The dinner, highlighted by unique moments, meaningful speeches, and a celebratory atmosphere, was also a fantastic opportunity to strengthen ties and exchange ideas with authorities, business leaders, and public-sector representatives who drive the France-Brazil relationship forward.

Congratulations to CCIFB-SP for its impeccable organization and for honoring Governor Tarcísio de Freitas with the 2025 Personality Award, a well-deserved recognition for his contributions to the development of the State of São Paulo and bilateral relations.

To CCIFB-SP and everyone involved: our heartfelt thanks for this unforgettable evening – here's to celebrating even more historical milestones!

Our partner Anne-Catherine Brunschwig conducted two Masterclasses on October 22 and 23, focused on setting up a branch in Brazil and the adaptation of business practices to the local market.

These events were organized by Business France, as part of preparations for the France-Brazil Economic Forum on Energy and Ecological Transition – Pre-COP 30.

The sessions provided a legal and strategic analysis of the partnership structures best suited for the Brazilian market, addressing key topics such as governance, cross-border taxation, local regulatory restrictions, and compliance mechanisms.

Congratulations and many thanks to Anne-Catherine Brunschwig for her excellent contribution and the clarity with which she shared her expertise!

We also thank the Business France teams for the perfect organization of these meetings.

See you on November 4!

Taking part in the French Tech Summit 2025 was, once again, an enriching experience for our team! The event brought together startups, companies, and technology experts in dynamic panels and a program focused on innovation and the future.

What made the event special for us? Beyond the debates on fascinating topics such as Artificial Intelligence, biotech for a sustainable Amazon, Women in Tech, and much more, we were delighted to reconnect with some of our clients who are at the forefront of digital and technological transformation. Seeing up close the innovative projects these companies are involved in was, without a doubt, inspiring.

The French Tech Summit once again highlighted the power of international collaboration and the positive impact it can generate. We are excited to continue following the innovations that will emerge from this rich exchange between France and Brazil.

Thank you, French Tech São Paulo — see you at the next edition!

A set of new rules that promise to simplify the relationship of foreigners and Brazilians living abroad was implemented in Brazil as of January 1, 2025.

The Central Bank of Brazil and the Securities and Exchange Commission of Brazil (CVM) published Joint Resolution No. 13/2024, which significantly modernizes the well-known Non-Resident Account (CND). This initiative seeks to make the business and investment environment more accessible and aligned with international practices.

The CND, at its core, is a bank account in Brazilian reais (BRL) intended for individuals or companies that do not have tax residency in Brazil. It functions as a channel to move funds, invest, and hold assets in the country of origin or of interest, even while living abroad. The innovations introduced by the new Resolution mark a shift toward administrative simplification.

Historically, operating a CND was surrounded by complexities, requiring, for example, a legal representative in Brazil for various operations and the execution of simultaneous and mandatory foreign-exchange procedures. Registration in the RDE-Portfolio system, previously mandatory with the Central Bank of Brazil (Bacen), also added layers of complexity. With the new regulation, the good news is that much of this bureaucracy will be eliminated. The elimination of the requirement for simultaneous FX operations, for instance, reduces costs and speeds up transactions for investments in the capital markets. Likewise, the requirement to register with RDE-Portfolio has been removed.

This modernization paves the way for the CND to become a much more flexible instrument. From now on, funds deposited may be invested directly in a variety of securities and other financial assets in the Brazilian market. Individuals, in certain scenarios and within certain limits, may even be exempted from the need to appoint a legal representative in the country. The goal is clear: to facilitate investment and wealth management without the heavy administrative burden of the past. This flexibility is also vital for those who change their tax residency, as it allows them to maintain investments in Brazil without being required to sell them or close positions.

However, it is crucial to understand that, although more streamlined, the new regime maintains certain important restrictions. It will still be prohibited to transfer investments or securities of non-residents in ways that are not expressly provided for in the regulations of the Central Bank of Brazil or the CVM. In addition, Joint Resolution 13 now expressly prohibits receiving, paying, and other financial movements in accounts held abroad from the CND, with specific exceptions for transactions related to forward, futures, and options contracts on agricultural products, provided they are contracted in Brazil by non-residents and in compliance with the applicable regulations. Compliance with strict Know Your Customer (KYC) and Anti-Money Laundering/Countering the Financing of Terrorism (AML/CFT) standards remains a non-negotiable priority.

This weekend, we had the honor of organizing a special day with the children of Lar Batista de Crianças, located in Cidade Tiradentes.

In addition to the financial support we provide to ensure the presence of psychologists who take care of these children’s emotional well-being, we wanted to do more. That’s why we dedicated this day to creating unique moments of joy and connection.

We would like to sincerely thank the team of GTLawyers volunteers: those who were present, running workshops and bringing smiles, as well as those who couldn’t be there but made sure to send gifts to the children.

Our gratitude also goes to the workers and educators at Lar Batista, who devote their time and care every day to transform the lives of these children.

And finally, a heartfelt thank you to the children, who filled us with joy and reminded us of the importance of giving, helping, and sharing.

The changes brought by the tax reform are expected to have a significant impact on the real estate market.

Do you know what the main points of attention will be and how to prepare for them?

Our partner, Estevão Gross, will address this topic during the webinar:

October 21st, at 5 PM.

Register now through the link below to secure your spot!

https://lnkd.in/eiVHcax3